Simplifying Fixed Income Attribution

One of the aspects of Portfolio Management that is sometimes misunderstood or over-complicated is Attribution. Specifically, Fixed Income Attribution. One of the toughest challenges faced by Portfolio Mangers, regardless of the size of their Portfolio or firm, is that they struggle to find existing Fixed Income Attribution Models that are suitable for their Portfolios. While some models are more focused on Yields and Shifts, others are more focused on Durations and Spreads. The solution that is looked for by Fixed Income Portfolio Managers needs to be flexible so that the Attribution Model truly reflects the Portfolio.

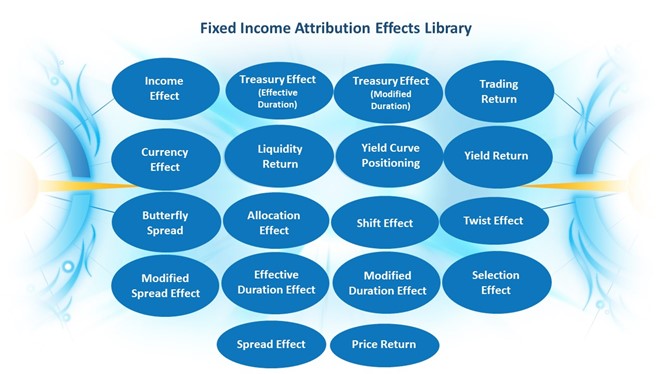

Accio Analytics’ current Attribution Effects Library has those illustrated in Figure 1. The concept is not to just simplify Fixed Income Attribution. The idea is to make it versatile and relevant, while being simple to create. Versatility is important for the evolving industry and types of Fixed Income securities, but also to the types of existing Fixed Income Portfolio s. Some Portfolio s are Yield heavy while others are more Duration based. Some are simply a unique combination of the two. Relevancy is paramount because the model needs to be suitable for the Portfolio’s mandate. Simplicity is critical because not every fixed income Portfolio is managed the same and the attribution model needs to be right for the Portfolio to be meaningful.

Figure 1

Another aspect that frustrates Portfolio Managers is that they are forced to choose between vendors who supply rigid solutions and using models that are not reflective of the Portfolio. Then the added expectation of using those models to analyze, evaluate, and explain the Portfolio’s performance using those rigid and unsuitable models.

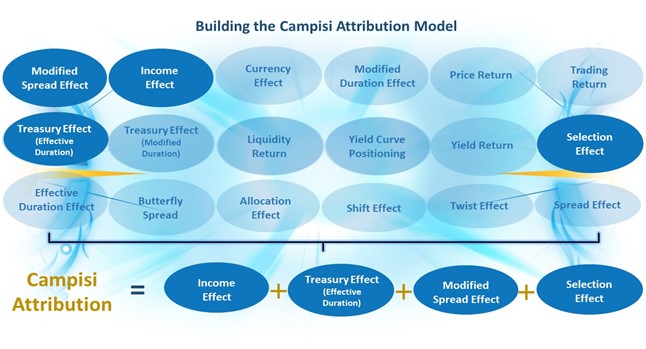

Utilizing Accio Analytics’ Library, you can easily and quickly construct your Fixed Income Attribution Model. For example, let’s look at the Campisi Attribution Model (Figure 2). While the mathematical model may seem complicated, it is broken into four ‘effects’:

Campisi Attribution Model = Income Effect + Treasury Effect + Spread Effect + Selection Effect

There are effects that are common amongst models, but some are only common by name or type. For Example, Treasury Effect is computed differently in different attribution models. A model may use the Effective Duration while another may prefer Modified Duration. Some models themselves maybe indifferent to which duration to use and defer that decision to the Portfolio Manager. As such, one would simply use the Duration that is preferred by them. In Accio Analytics library, there are two Treasury Effects: Treasury Effect (Effective Duration) and Treasury Effect (Modified Duration). The Campisi Model uses the Treasury Effect (Effective Duration).

Similar to the Treasury Effect, the Spread Effect used by the Campisi Attribution Model is different from the Spread Effects used by other models. The Spread Effect that is used in Accio Analytics’ Campisi Attribution is referred to as the Modified Spread Effect in the Accio Analytics’ Effects Library. To final Campisi Attribution Model is highlighted in Figure 2.

Figure 2

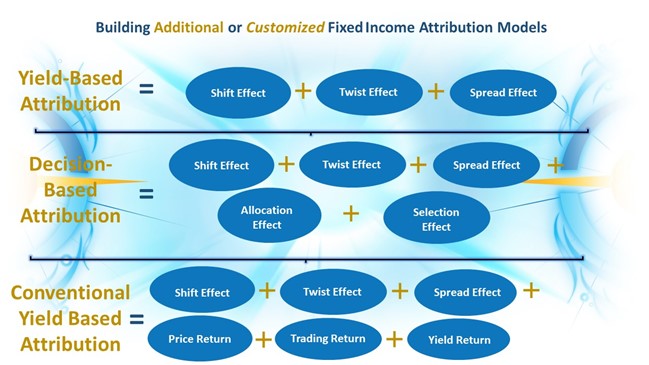

These scenarios are now commonplace in the investment industry and Accio Analytics is built to address them and has designed its platform to ensure that the flexibility you need is there. Figure 3 highlights the simplicity by which other Fixed Income Attribution Models may be created to be suitable for your Portfolio and strategy.

Figure 3

Accio Analytics has the flexibility and architecture to support complex Fixed Income Attribution in a simplified manner by focusing on the individual effects. By doing so, it is simpler and easier to decide whether the Attribution Model is relevant or not. To make your attribution model relevant, if you need to change existing Effects in the library or create new ones, you can. This is Accio Analytics’ approach to making your analytics more meaningful and relevant, so you can better evaluate and explain your investment strategy and your Portfolio’s performance.

Why is this important?

This is important because, as we discussed earlier, flexibility to ensure the Attribution Model is relevant to and reflective of the portfolio’s strategy is paramount. However, this flexibility can lead to confusion on how one should build the model and what effects should be included in the that model. As the purpose of attribution is being able to explain your relative return to the benchmark, it is important to have all the effects that would best explain that relative performance in its entirety.

That said, the flexibility we have been discussing, is two-fold: flexibility to choose the effects that are relevant and ensure the effects chosen can be modified to provide consistency throughout your analysis. Continuing with the earlier example of duration, the use of duration should be consistent with the overall management of the Portfolio. For true value-add from your attribution model, you would need to be using the same duration throughout your analysis. For example, if you are preferring to use Modified Duration as part of your overall portfolio analysis, then it won’t be as meaningful to use Effective Duration in the attribution model. You would need a solution that allows you to tweak effects to provide that consistency throughout your analysis.

Now circling back to relevancy, the flexibility is important to ensure that all aspects of relative return be explained. For example, while your investment strategy may be duration-based, you may not have a complete explanation without including some aspect of yield in your attribution model as it may be a more contributing factor to the relative performance of the portfolio. Again, Accio Analytics is simply focused on providing you the tools and flexibility to ensure your attribution analysis is explainable in its entirety.

Why else is this important to you and your firm?

Anyone managing or analysing Fixed Income securities will be able to have more meaningful conversations about investment strategies and decisions with their CIO and Investment Strategy teams, as well as those in client-facing roles. Those in client-facing roles can also use attribution results to serve their clients better by giving more meaningful, detailed and insightful advice to them and review their clients’ portfolios in a more meaningful manner. This approach provides the firm value that is realized internally and may be communicated externally to the firms’ clients, furthering their experience with the firm.